Related Stories

April 9, 2024

Title: The Alarming Rise of Identity Theft: A 2024 Perspective In recent years, the threat…

July 27, 2022

IRS Fresh Start Initiative Program, resolving IRS tax debts. Do You Need a Fresh Start…

June 9, 2022

IRS First Time Penalty Abatement – FTA The first-time penalty abatement (FTA) waiver is an…

March 26, 2022

If you filed a chapter 7 bankruptcy, look into filling IRS form 982 When you…

March 26, 2022

DID SOMEONE FILE FOR UNEMPLOYMENT BENEFITS UNDER YOUR NAME? If you discover that someone has…

February 3, 2022

RICO suit, McKinsey In a decision last week, the Court of Appeals for the Second…

December 17, 2021

BEWARE OF USING MONEY FROM YOUR IRA OR 401(K) TO PAY DEBTS This can be…

December 17, 2021

How to Spot Student Loan Scams. Things you can do to protect yourself. “Enroll now…

April 9, 2024

Title: The Alarming Rise of Identity Theft: A 2024 Perspective In recent years, the threat…

July 27, 2022

IRS Fresh Start Initiative Program, resolving IRS tax debts. Do You Need a Fresh Start…

June 9, 2022

IRS First Time Penalty Abatement – FTA The first-time penalty abatement (FTA) waiver is an…

March 26, 2022

If you filed a chapter 7 bankruptcy, look into filling IRS form 982 When you…

March 26, 2022

DID SOMEONE FILE FOR UNEMPLOYMENT BENEFITS UNDER YOUR NAME? If you discover that someone has…

February 3, 2022

RICO suit, McKinsey In a decision last week, the Court of Appeals for the Second…

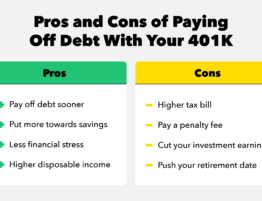

December 17, 2021

BEWARE OF USING MONEY FROM YOUR IRA OR 401(K) TO PAY DEBTS This can be…

December 17, 2021

How to Spot Student Loan Scams. Things you can do to protect yourself. “Enroll now…